CapitalRise Hosts Investor Drinks Evening at The Whiteley

On 23rd May, CapitalRise hosted our spring drinks event at the exclusive Whiteley Marketing Suite in West London. The evening was attended by 50 of our current investors plus some special guests, including keynote speaker, Tom Bill (Head of UK Residential Research, Knight Frank). Tom joined Uma Rajah, CapitalRise CEO, for a very informative presentation on the PCL (Prime Central London) market, followed by a Q&A with our guests. All of this was accompanied by English sparkling wine and a choice of canapés.

The Whiteley, whose Marketing Suite was the setting for the evening, sees the high-end redevelopment of the iconic department store, which first opened in 1911. The landmark project brings together some of the most talented architects and developers, who are breathing new life into this architectural gem. The masterplan includes a blend of luxurious private residences, the UK’s first Six Senses hotel, and choice restaurants, leisure facilities and retailers.

Uma provided the context for the evening, with CapitalRise having had an incredibly successful year to date, recently reaching the milestones of £280m total of loans agreed and £132m capital and returns paid to investors. Uma went on to explain that we expect continuing exponential increases in the number of investment opportunities into 2023, and that we are excited to see strong growth for the business in the coming year.

Uma then introduced Tom Bill. In his role as Head of UK Residential Research he produces reports that include Knight Frank’s flagship Prime London indices, the Super Prime London Insight and the London Residential Review. He writes regular articles on how economic and political events shape the UK housing market and has contributed to The Wealth Report, Active Capital and the Global Cities report.

His talk covered a range of topics relating to the PCL market and the current trends. Some key takeaways included:

Inflation Rates in UK

- Inflation rate trends in the UK has historically been influenced by the Natural Gas Index

- Moving on from the significant increase in gas prices from 2021-22, we have more recently seen a dramatic decrease in the natural gas prices.

- As such, inflation is expected follow this downward trend in gas prices, which we are starting to see signs of recently.

Mortgage market moves on from the Mini Budget

- Mortgage rates have started to decline back down to the summer 2022 (pre-Mini Budget) levels.

- That is despite bank rates having continued to rise since Rishi Sunak becomes PM in October 2022.

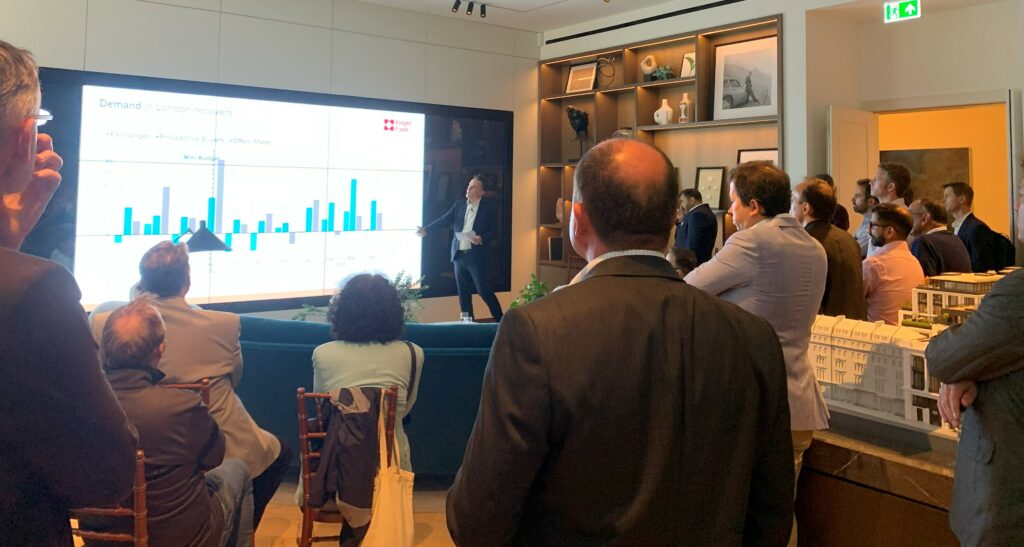

Demand in London recovers

- Compared to the 5-year average, the demand in London property has recovered.

- Tom demonstrated that property exchanges, and the number of prospective buyers and offers made in London have all recovered significantly, especially in the last 4 months (Jan-April 2023) showing the increasing demand in the city.

London: Outstanding mortgage debt

- Showing a heat map of outstanding mortgage debt by postcode sector (as a proportion of total property value), central London showed significantly lower levels of mortgage debt than some areas of outer London.

- Tom made the point that equity-rich markets are more immune from mortgage volatility, enhancing the fact that Prime Central London is more resilient due to the wealth of the buyers.

£10m-plus transactions in London are increasing

- Both the value and number of £10m+ transactions has increased over the last 3 years.

- This follows a period of decline in these values from 2015-19.

- However, with the recovery seen since 2020, the future is looking more positive for £10m+ properties in London.

Overseas travel to London recovers post-Covid

- Looking at Heathrow passenger arrivals vs. four years ago, we are now more or less back to pre-covid numbers from most regions.

- APAC has not quite reached the pre-covid arrival of passengers into London yet, but it has been significantly rising following recent ‘unlockings’ in the region.

- This is expected to increase international demand for PCL property once again.

Impact of the decreased value of the Pound

- While having negative impacts in other areas, the decrease in the value of the Pound has effectively offered a currency discount for overseas buyers.

- Looking at the discount since July 2014 in PCL, we see a 21% discount for Euro buyers, 31% for Chinese Yuan, and 37% for Australian and US Dollars.

- This is also expected to increase demand from overseas buyers.

London in recovery mode vs. Country

- Tom compared the ‘London’ property market to the ‘Country’ market (e.g. Home Counties, Cotswolds etc.).

- By comparing the five year average, the data showed London to be greater – in some case significantly so – than the country in all areas such as new applicants, instructions, viewings, offers made and exchanges.

- This again proves the resilience to the Prime Central London Property market.

Sales market forecast: PCL to outperform UK overall

- Overall it is looking very positive for all the property sales market forecasts over the next 5 years.

- The UK overall is forecast for a 2.5% increase, cumulative 2023-7. However, Prime Central London is forecast for 8.1% sales market increase in the same time period.

The Political Outlook

- With a General Election on the horizon, parties are debating the building of new homes with the aim of reducing prices. This is likely to become a major topic in the upcoming campaigns.

- For instance, the Conservatives have been accused of ‘watering down’ their pledge to build 300k new homes.

- However, Tom points out that – while these pledges may sound good in a manifesto – the number of new homes that will or won’t be build, and the impact on property prices, will be determined by market demand, not government-issued targets. The actual number that will be built is yet to be seen…

Following the talks, Uma and Tom hosted an illuminating Q&A. Our investors asked questions on a range of topics including: the trends in the 2nd tier London markets just below PCL, CapitalRise’s current Seedrs raise, and the impact of a Labour election victory on the sector.

We would like to say a big thank you to our partners at The Whiteley, Finchatton and Knight Frank – and of course to our fantastic investors for making the evening both enjoyable and informative. We hope to see you at the next CapitalRise event!